{kind=link}

| Getting your Trinity Audio player ready... |

Written by BISP IB Economics Teacher Hugh Pollock

Long answer questions can be intimidating for students preparing for their International Baccalaureate (IB) Economics exams. These questions often require a deeper understanding of the material and the ability to apply economic concepts to real-world scenarios. However, with proper preparation and a clear strategy, it is possible to succeed on these questions and earn a high score on your IB Economics paper. In this article, BISP IB Economics Teacher Mr. Hugh Pollock provides tips on how to approach long answer questions in the IB Economics Paper 1 exam and increase your chances of success.

Paper 1 in IB Economics is an options paper. Students are presented with three questions from which they choose one question. Each question has two parts: part (a) and part (b). Part (a) is 10 marks while part (b) is 15 marks. The challenge for students in these types of questions is to structure their answers correctly, something many students find difficult. I will outline what is expected to achieve excellence (Grade 7) in questions like this.

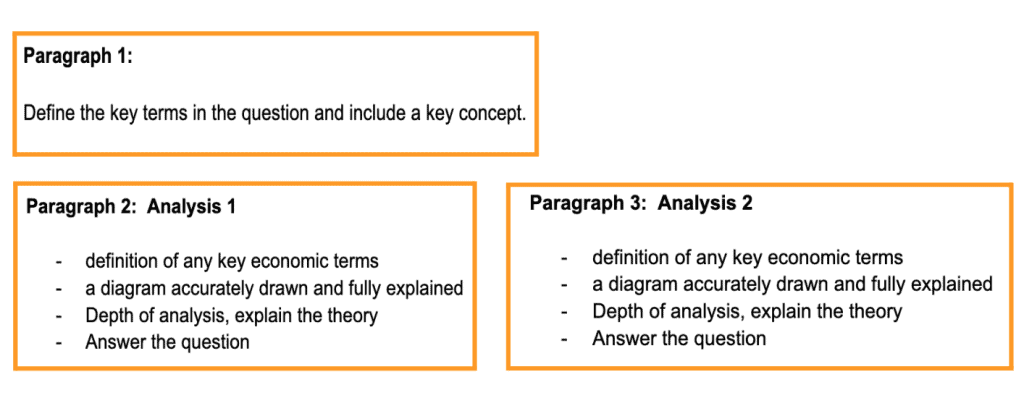

10 Mark Questions

The 10-mark question will always follow the same structure. Here is an example below. Explain the concepts of consumer surplus and producer surplus (10 marks)

The 10-mark question will expect you to make two analysis points. The question usually specifies this but if it does not, assume two analysis points are required. This is the structure to follow to achieve high marks.

Example of one analysis point

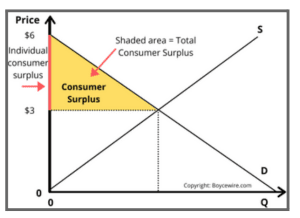

Consumer surplus is the difference between what the consumer is willing to pay and actually pays. For example, if a consumer is willing to pay $5 for a pen but only pays $2, his consumer surplus would be $3 { $5 – $2 = $3}. This can be illustrated using a diagram.

Graphically the consumer surplus is represented by the area above the equilibrium price ($3) and below the demand curve (D). This means all the consumers above $3 are willing to pay a higher price and therefore receive a benefit from paying for the good. Total consumer surplus can be calculated by finding the area of the yellow triangle. Total consumer surplus is the sum of all individual consumer surpluses. Consumers aim to always seek to maximise consumer surplus or in other words want to pay the lowest price possible.

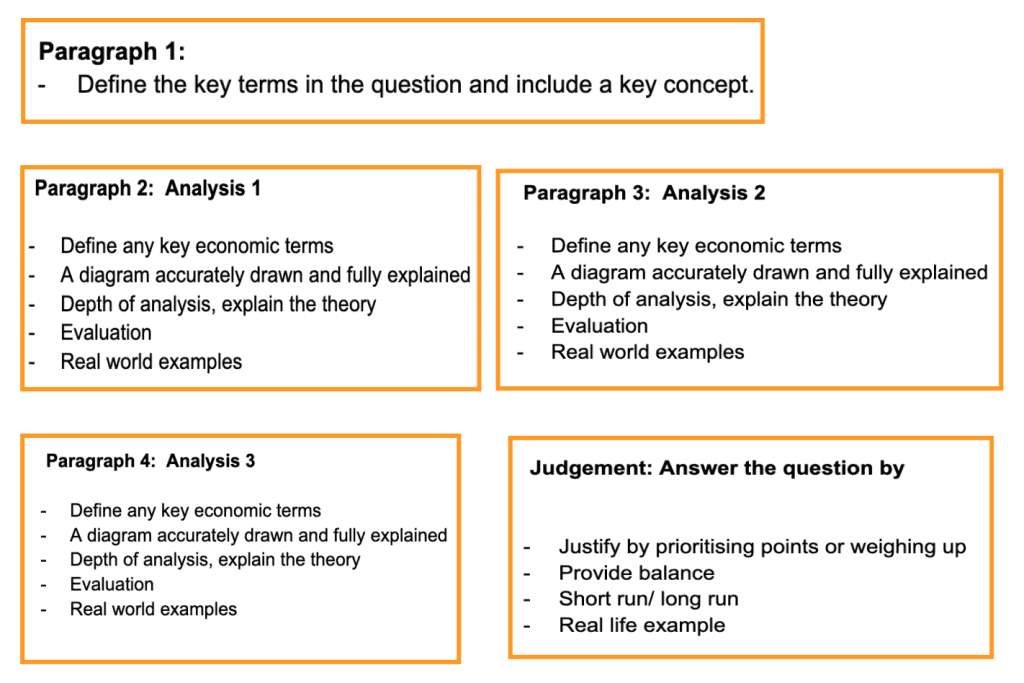

15 Mark Questions

The 15 marks question will always be one of two styles:

Pros and cons: Explain the consequences of introducing a price ceiling on stakeholders (15 marks).

Multi-policy: Evaluate the view that the most effective way in which the government can encourage the consumption of merit goods is through direct Provision (15 marks).

This is a lot more challenging but is still very achievable if the structure is followed:

Example of one analysis point

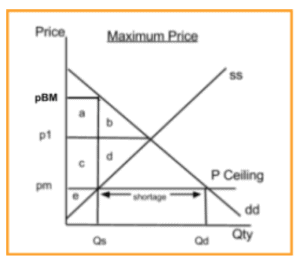

Explain the consequences of introducing a price ceiling on stakeholders (15 marks).

A price ceiling or maximum price is a legal limit set by the government on the price a producer can place on a good and service. (definition). This is usually set on goods that are seen as necessities for example rent and food. However, a price ceiling leads to allocative inefficiency. Allocative efficiency occurs when the quantity supplied does not equal the quantity demanded. Or in the other words the marginal benefit does not equal the marginal cost. Marginal benefit the benefit a consumer receives from consuming one extra unit of a good or service. Marginal cost the extra cost of producing one extra unit of a good. (analysis)

The diagram illustrates this:

Before the price ceiling the equilibrium price was P1. The introduction of the price ceiling (pm) creates a shortage of Qd – Qs. The lower price causes an expansion in demand and a contraction in supply. (diagram fully explained)

Consumer surplus is the difference between what a consumer is willing to pay and actually pays. Consumer surplus before the price ceiling was the area ( a + b). After the price ceiling, it is the area (a + c). It is not clear if consumers gain or lose from the introduction of the price ceiling looking at the diagram. However, the shortage means consumers will have to queue for the good or service meaning time is being wasted. Also, some consumers will get access to the product and benefit, however, the shortage means some consumers will lose out and cause them to pay black market prices (pBM) which will be well above the equilibrium price before the introduction of the price ceiling. So to answer the question, do consumers as a stakeholder win or lose, the answer is it depends. (evaluation)

A real-life example of this is in Mumbai, India. Rents have had the same maximum price since 1949. Some tenants are paying 500 rupees a month for an apartment, they should be paying 100,000 rupees, leading to a chronic shortage of accommodation in the rental space.

Finally, in the final paragraph answer the question that is asked by making a judgement. A common mistake here is for students to summarise. This is not what is expected. Examiners want to see the student answer the question that was asked. To write a good judgement, students should prioritise their points made, recognise nothing is certain in economics by providing balance and look at short-run and long-run impacts. This will ensure a well-written and structured essay.